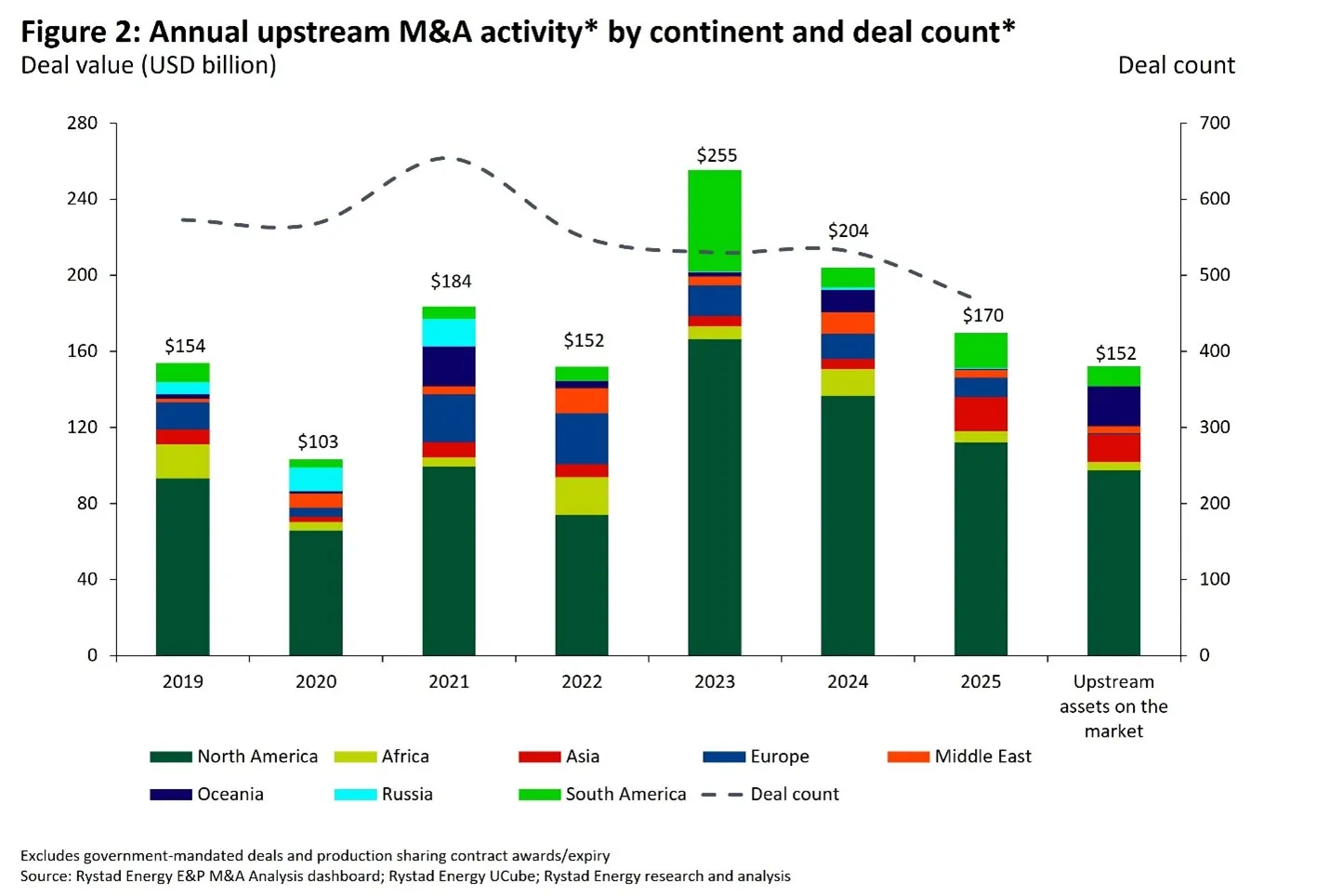

Global upstream merger-and-acquisition (M&A) activity is expected to be lower in 2026 than in 2025, with nearly $152 billion-worth of opportunities on the market as of January this year, according to analysis by Rystad Energy. Timing and execution will determine whether several mega deals will go through, with numerous high value assets still on the market waiting for the right buyers.

Here is Rystad Energy’s market update from Atul Raina, vice president, oil and gas M&A:

“Rystad Energy expects North America to remain the clear anchor for upstream M&A activity in 2026, with deal flow increasingly shaped by a new phase of a ‘merger of equals’ consolidation among small- and mid-cap listed US shale producers. This is further supported by ample private E&P capital yet to be deployed, ongoing consolidation in Canada’s Montney shale, and rising interest in gas and LNG-linked assets—particularly from Asian buyers seeking long-term security of supply.

By contrast, international M&A outlook remains uneven. While the pipeline of opportunities is sizeable, activity is concentrated around a small number of high-value and often complex transactions, limiting broader deal momentum. National oil companies from the Middle East, Asia, and South America are likely to be among more active participants, reflecting their continued appetite for scale and international exposure at a time when many IOCs remain selective.”

Global upstream M&A activity dipped 17% year-on-year (YoY) to approximately $170 billion in 2025, with deal count decreasing 12% to 466. Consolidation within North American shale plays, LNG investments across US and Argentina, and majors’ spinning off assets in Asia and the UK to form new regional joint ventures emerged as key themes last year. A few key deals across these themes include SM Energy and Civitas’ merger, Cenovus Energy’s acquisition of MEG Energy, a Blackstone-led consortium’s acquisition of a 49.9% stake in the Port Arthur LNG phase 2 project from Sempra Infrastructure Partners (SIP), Eni and Petronas merging certain assets in Indonesia and Malaysia, and TotalEnergies merging its UK operations with NeoNext Energy to form NeoNext+.

Key early year updates include Coterra Energy and Devon Energy reportedly evaluating a potential merger, while Mitsubishi has announced a $7.5 billion acquisition of Aethon Energy. Internationally, activity is expected to remain uncertain. The pipeline of investment opportunities stands at $55 billion, but this includes $23.5 billion attributed to a potential sale of Santos as the company remains open to offers, and $17 billion for Lukoil’s international upstream assets. Additionally, national oil companies (NOCs) including ADNOC, Saudi Aramco, Petronas, Petrobras, Pertamina and Ecopetrol could emerge as key buyers in the coming year.

Overall, North America led activity in 2025, accounting for more than $112 billion – or 66% – of total deal value. A similar regression was seen across most regions. Deal value in Africa dropped 57% YoY to $6 billion, Europe saw a 24% YoY decrease to around $10 billion, the Middle East recorded a 65% fall to nearly $4 billion, Oceania saw a 96% drop to around $435 million, and Russia observed a 25% decrease to nearly $750 million. This overall global decline is primarily attributed to low and volatile oil prices during 2025 that had a lasting negative impact on the buyer-seller spread. Brent prices declined from around $79 per barrel in January last year to around $65 per barrel in May, surged back to more than $70 per barrel in June and July, and finally settled around $63 per barrel by the end of December.

During the same time, West Texas Intermediate (WTI) prices started last year at $75 per barrel and settled around $58 per barrel in December.

M&A activity only increased in Asia and South America. Deal value in Asia more than tripled to $18 billion, driven by the Eni and Petronas joint-venture formation, while deal value in South America increased 71% YoY to $18.3 billion on the back of several LNG and Vaca Muerta focused deals in Argentina.

This year’s global LNG M&A activity is expected to remain below last year’s level, but it is still projected to be robust, with more than $8.6 billion-worth of LNG infrastructure assets already available on the market. This figure excludes the potential sale of Santos, after an ADNOC-led consortium withdrew its $23.6 billion bid. Additionally, $2.5 billion-worth of upstream assets that feed to LNG plants are also up for sale. Among potential transactions, Energy Transfer is reportedly exploring the divestment of an 80% stake in the pre-FID Lake Charles LNG project. In Argentina, YPF is reportedly seeking partners for its Argentina LNG project. Geographically, the US is likely to continue leading deal activity. Meanwhile, Middle Eastern NOCs such as Saudi Aramco and ADNOC are expected to remain active, having already acquired LNG assets globally and continuing to emerge as potential buyers for key opportunities.

“Join the companies that smart energy professionals follow – because when you’re featured on OGV, the industry pays attention.”